What Is Stagflation and Why It Matters Now

Stagflation happens when the economy slows but prices keep rising. It’s the worst of both worlds—high inflation mixed with low or no growth. It causes problems for businesses, consumers, and policymakers alike.

We’re seeing signs of stagflation today. As will be exhibited momentarily, both the manufacturing and services ISM data released this month display warnings signs of stagflation. Manufacturing is slowing after only two months of modest growth, however prices are soaring, and new tariffs according to economists are making goods more expensive. At the same time, consumer demand is weakening, which could reduce economic growth even more.

This rare combo is exactly what the latest economic data is showing. Supply chains are under stress, manufacturing is contracting again, and price pressures aren’t going away. This however does indicate that the Federal Reserve will need to act promptly to prevent further fallout. They have already began the process of unwinding QT, which started this week and the market is now predicting 4 rate cuts this year. Let’s break it down.

Manufacturing Data Screams Warning Signs

In March 2025, the U.S. Manufacturing PMI fell to 49. That means contraction. It’s lower than February’s 50.3 and even below December’s number. Orders are shrinking faster for the second month in a row. That’s a huge red flag.

Prices, though? They’re red-hot. The prices index jumped to 69.4. That’s six straight months of price increases. Supply costs are climbing. This isn’t seasonal or short-term—it’s a pattern.

Exports also slipped to 49.6, showing contraction. Imports, however, grew slightly to 50.1. It’s a mismatch with the aims of last months implemented tariffs. We’re buying more than we’re selling. That adds pressure to U.S. manufacturers already fighting high input costs.

Services Sector Tells the Same Story

The divergence between services and manufacturing, paired with inflation and stagnant employment, illustrates a

stagflationary environment. Stagflation occurs when economic growth stalls while inflation and unemployment rise—precisely what current indicators reflect. There is not enough data available to indicate a complete trend of stagflation, but the early warnings signs are clearly present in the latest data.

Tariffs Raise Prices Across the Board

Now enter tariffs. On April 5, a new 10% global tariff hits. Reciprocal tariffs go into effect April 9. China gets hit hardest. After stacking the new 34% rate on top of earlier ones,

Chinese imports will face a 54% base tariff. Citing national security and the trade deficit, President Trump invoked the

International Emergency Economic Powers Act (IEEPA). His administration aims to shield U.S. manufacturing by limiting foreign competition and raising barriers to imported goods.

It is worth advising however that tariffs also drive up input costs for U.S. Manufacturers though. Imported machinery, parts, and materials—many of which are critical to domestic production—now come at significantly higher prices. Inflation at the production level may accelerate, exacerbating stagflation risks. Manufacturing output is shrinking. Services hiring is falling. Prices in both sectors are rising rapidly. The economy shows signs of cooling while cost pressures intensify across supply chains.

Some goods could see tariffs of over 70%. It’s the biggest trade barrier since the 1930s.

These tariffs will push companies to rethink sourcing. During Trump’s first term, some companies, like Nike, diversified away from China but shifted to other low-cost countries like Vietnam and India. But where can they go? The alternatives to China now face high tariffs too. And China’s trade retaliation adds more stress.

Other countries aren’t spared. Vietnam faces 46%, Bangladesh 37%, India 27%, Cambodia 49%. Even Canadian auto imports get a 25% tariff. These aren’t just tweaks—they reshape global supply chains overnight.

In retaliation, it was announced today that

China is imposing its own 34% tariffs on U.S. goods. The aggressive escalatory response from china is extremely concerning, as it is a worst case scenario playing out. The odds of a near-term deal to end the trade war now seems less probabilistic. China is also adding export controls on rare earth exports and blocking certain U.S. farm imports. The trade war is heating up fast—and supply chains are caught in the middle.

Even with some exemptions, companies are in limbo. Rules can change quickly as this is a dynamic situation. Foreign concessions may lift tariffs, but that’s uncertain. Businesses can’t plan long-term strategies in this environment.

De Minimis Crackdown Chokes E-Commerce

Another big change: the end of the de minimis rule for Chinese goods. This rule let low-value items skip duties and customs. It powered a surge in cheap online shopping from China.

That ends on May 2.

Parcels under $800 will now pay either a 30% tariff or a $25 fee—going up to $50 on June 1. Millions of shipments will face delays and higher costs.

Trump paused the rule earlier this year, then brought it back, and now it’s ending again. This back-and-forth has overwhelmed U.S. Customs and spooked small parcel carriers.

The Impact on the US Dollar

In response to these developments, expectations for Federal Reserve interest rate cuts have increased, with four rate cuts now priced in, beginning in June. This anticipation has contributed to the dollar's depreciation, as lower interest rates typically make a currency less attractive to investors.

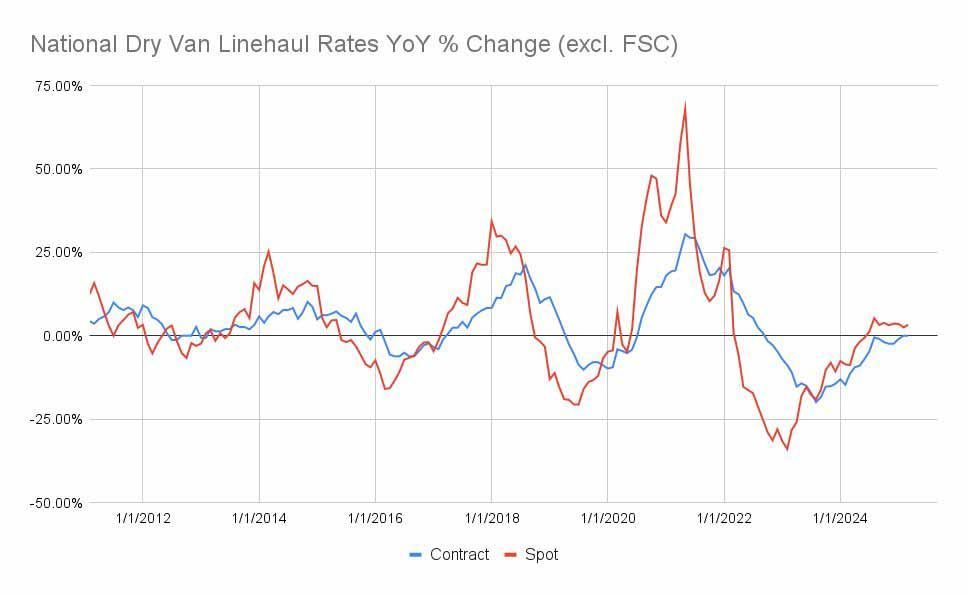

The Impact on Freight Rates

More recently, both contract and spot rates have stabilized, showing modest YoY growth in 2024. This suggests that the market is recovering but not yet experiencing the strong upward momentum seen in previous cycles. Several macroeconomic factors are influencing this trend, including the weakening U.S. dollar, which historically supports exports and could lead to increased freight demand. However, if global trade remains weak, the impact on domestic trucking volumes may be limited. Long term however if the Trump tariffs are successful in their underlying goal, then domestic transportation demand will increase significantly.

Flatbed freight continues to experience a surge in demand, with the flatbed load-to-truck ratio jumping 16.9% in the past week, signaling tightening capacity in the segment. This rising demand has translated into a 4% increase in flatbed spot rates, reinforcing the strength of the market. Over the past year, the flatbed segment has seen explosive growth, with load-to-truck ratios up 129.5% YoY, highlighting persistent demand for construction materials, industrial freight, and oversized shipments. However, while flatbed spot rates have ticked up in the short term, their stability over the past month suggests a potential ceiling unless further capacity constraints emerge.

Meanwhile, reefer freight has seen an even greater surge in demand, with the reefer load-to-truck ratio climbing 23% week-over-week. Despite this significant imbalance between available freight and capacity, reefer spot rates remain flat, indicating that carriers have not yet been able to push through higher pricing. This could be due to lingering excess capacity in the segment or seasonal factors keeping shippers hesitant to accept rate hikes. Over the longer term, if demand continues to rise—particularly as produce season ramps up—reefer rates could begin to reflect the tightening market. However, for now, reefer carriers are facing a paradox of strong freight volumes but limited rate movement.

Looking ahead, the freight market appears to be in a phase of

cautious optimism rather than a strong rebound. While contract rates may continue to rise gradually, spot rates seem more vulnerable to stagnation unless economic conditions improve. Consumer spending and industrial production will be key determinants, as freight demand is tightly linked to broader economic activity. The Federal Reserve’s potential interest rate cuts later this year could provide a stimulus, boosting freight volumes and supporting higher rates. However, without a clear catalyst for tightening capacity, trucking rates are likely to remain range-bound in the near term.